On Monday June 9th, the Ohio Power Siting Board approved the application of the Socrates South Power Generation Project. The announcement is the usual sparse and glyphic announcement from a state regulatory body.

.png?width=50&name=34C0AE28-DE08-4066-A0A0-4EE54E5C1C9D_1_201_a%20(1).png)

This week, Halcyon shipped the 12th monthly update to its Gas Power Plant Tracker.

We initiated this data series in July 2025, tracking 134 plants totalling 65.6 gigawatts under development. More than half of that capacity was attributed to the combined-cycle gas plants that have been the backbone of U.S. firm bulk generation for decades. Simple cycle turbines made up much of the remainder, with less than two gigawatts of reciprocating internal combustion engines (RICE) and a handful of older thermal plant conversions comprising the rest.

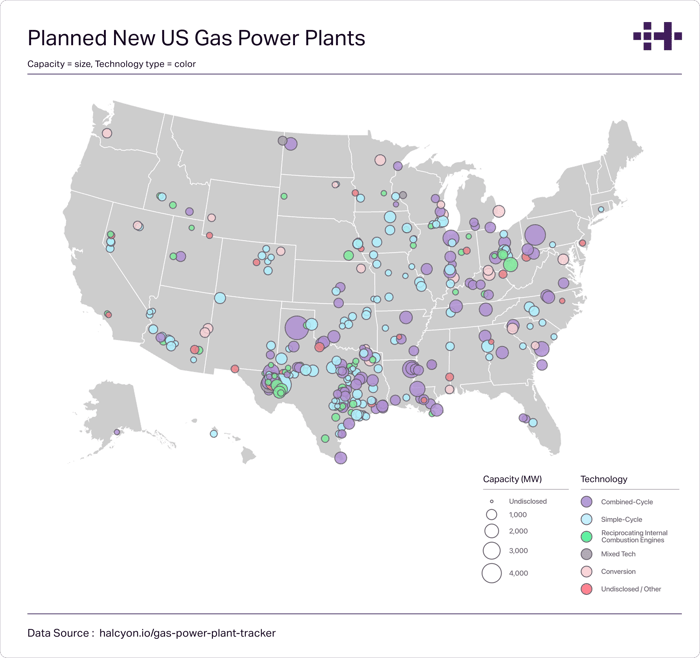

Twelve months later, Halcyon now tracks 382 gas power assets under development, and more than 212 gigawatts of potential capacity — enough to increase today’s installed gas plant base by more than 35%. Forty-four out of 50 U.S. states are planning a gas plant; New England is the only region without significant activity. On the map, you can see an intense cluster of assets in Texas leading into a broad swath of assets in the lower Mississippi, Mid-Continent and Ohio River Valley.

What has changed, one year on? Magnitude, obviously, with more than three times as many tracked assets as a year ago. But, that expansion is due to both a massively expanding market, as well as an increasingly sophisticated Halcyon toolset to capture, identify, and classify assets across an expanding catalog of more than seven million regulatory documents. Put simply, capturing air permits helps you find more gas plants. The increase in assets identified through air permits isn’t just about collection — it is also about recency. Most of these assets were filed in the last six months; they are not backlogged.

Asset mix has changed, too. Halcyon now tracks nearly as many planned installations of gas-fired reciprocating internal combustion engines (89) as combined cycle plants (101), and nearly 10 times more known generation capacity from RICE assets as a year ago (18.3 gigawatts, up from 1.85 gigawatts in June 2025).

There is now significant activity behind the meter. Halcyon tracks 31 assets which are specifically as ‘behind the meter’ for large load customers, which, in 2026, means almost exclusively data centers.

Importantly, the data show just how acute this wave of gas power plant development is today (and may be in the future too). Halcyon expects less than seven gigawatts of plant commissioning in 2026, roughly double that much next year, and double again sustained each year from 2028 through 2030. After that the pipeline drops sharply and trails off: Halcyon expects only a single 400-megawatt combined cycle plant to be commissioned by 2034.

Speed to power is the paramount market concern, and we can clearly see this urgency in the data. Last year, only 190 megawatts of RICE generating capacity came online; this year that figure will be 3.6 gigawatts, and 3.9 gigawatts in 2027. By 2028, long lead time combined cycle plants will be less than half of expected commissioning.

-Jun-17-2026-10-59-06-2177-PM.png?width=700&height=394&name=unnamed%20(3)-Jun-17-2026-10-59-06-2177-PM.png)

Of course this sort of Gaussian distribution also moves over time. More assets could be announced in the coming months that add to the leading edge of this chart, contributing to another year or two of sustained buildout. And as more filings arrive for announced assets, more timelines (and configurations, and vendors, and delays, and cancellations, and everything else) become evident as well. The shapes change both by moving, and by firming up.

A year of iteration is a sufficient interval for reflecting on processes and outcomes. On both fronts, the work you see here is a start, but it is more the end of the beginning than the beginning of the end of what can be built. In the past year we have added environmental equipment, plant engineers, power offtakers, and points of interconnection among other information. This month, we added contracted capacity details.

What comes next? More of everything: more data sources, more examination of existing known assets, more achieved depth of understanding of those assets, and more connection between those assets and the grid. That last bit is important, to us and to customers. No power asset lives in a vacuum, which is why Halcyon already tracks substations and battery energy storage assets, often with specific relation to this powerplant and/or that data center.

It is why we also track, in detail, the commercial arrangements by which today’s hyperscale assets connect to the grid via our Large Load Tariff Tracker. A quote from Meta Platforms’ filing this week in Missouri tells us why. Meta (filing as Velvet Tech Services LLC) requested to be party to utility Every Metro’s annual update to its Integrated Resource Plan. As it says, “Velvet has the potential to be one of Evergy’s largest customers, such that it has an interest in this proceeding different from that of the general public.” Today’s demands are too large for the system as it is.

Which means that the system is being built anew right now. More than 200 gigawatts of planned gas generation assets are just one manifestation of a system being rebuilt, at every level.

The Halcyon Gas Power Plant tracker is here.

Subscribe for more content like this; reach out with questions: sayhi@halcyon.io; follow us on LinkedIn and Twitter